My Cart 0

My Cart 0

We talked about how to save more money in the previous article. Now let’s talk about something that’s less fun but equally important: how to pay off debt.

We’ll all land in debt one way or another (that is of course, unless you have the backing of a trust fund), perhaps most commonly through student or housing loans. But there are other more pesky variants of debt, like credit card debts with exorbitant interest rates, or debts borne out of circumstance, such as an unexpected medical bill.

Debts are no fun and they literally take the life force out of you.

Unfortunately, there isn’t a magic wand you can wave to make your debts go away. But you can deal with debt in smarter ways to make it go away quicker.

Before we get into today’s debt mangement strategies proper, let’s begin with some hard truths.

Look at your debts squarely

When there is a mountain of debt piling up every month, the last thing anyone wants to do is to look at the number and feel depressed all over again.

But the first step in dealing with your debts is to look at it squarely. Say goodbye to debt denial.

From there, work out the reasons why you landed in debt. Was it poor spending habits? Consider canceling your credit card. Was it a lack of forward planning? Maybe speak to someone whose more financiall savvy to learn what you can do. Was it because you didn’t have a large enough Start building a substantial fund now. Basically, identify the reason and find the right remedy for it.

Once you have the numbers down, it’s time to work out a game plan. We did some research and found these two popular strategies that might help you eliminate debt quicker.

#1 Debt Avalanche Method

Following this method, you should pay off accounts starting from the one with the highest interest rate.

So here’s what you need to do.

- Make the minimum payment on all accounts

- Pay however more you can on the account with the highest interest rate

- Once you’ve settled your debts on that account, move onto the account with the second highest interest rate by paying the minimum amount + what you were paying for the settled account + any extra amount

This method makes sure you tackle the account with the highest interest first, so you incurr less damage at the end of the day.

#2 Debt Snowball Method

One of the downsides of the debt avalanche method is that you might not feel like you’re making progress, especially if you’re dealing with larger debt accounts first. It’ll take a longer time before you can tick anything off your list.

If you’re someone that functions better when you feel motivated and accomplished, consider the debt snowball method.

Following this method, deal with the account with the lowest balance first, then work your way up.

- Make the minimum payment on all accounts

- Pay however more you can on the account with the lowest balance

- Once you’ve settled your debts on that account, move onto the account with the second lowest balance by paying the minimum amount + what you were paying for the settled account + any extra amount

You can accumulate small wins along the way when you use this method, hence the name snowball.

However, do note that this method will mean delaying payment on the account with the highest interest rate. You will end up incurring more costs at the end of the day. Ultimately, you should know which method works best for you to deal with your debt successfully.

In the meantime, save more, earn more, and get to work chipping away at your debt!

Follow us on Telegram, Instagram, Facebook and Linkedin for more investment tips coming up!

What happened in markets this week, and what are analysts talking about?

iFast

To recap, iFast reported its results in April with a record net profit of S$8.8m in 1Q (2.5x from a year ago); on the back of a 51.4% rise in revenue. Assets under admin (AUA) also grew to a new record of S$16.1b. Link to results ppt

• UBS; Aakash: Initiate BUY with TP of S$10. While at first glance, iFast is expensive at 48x Forward PE, however, the House believes that near-term growth is not priced in, not to mention the potential hockey stick growth which the House believes may be possible given the scalability of the business. The House believes iFast may enjoy strong growth given (1) its recent history of rapid 20%+ AUA growth; (2) Early experiences of mature peers; (3) Structural Asian wealth management growth opportunity in SG/China; (4) Greater acceptance of online platforms and (5) Room to grow market share in 5 key markets.

Riverstone Holdings

• CIMB; Ong Khang Chuen: Maintain BUY with a lower TP of S$1.80. Continue to like Riverstone for its strong earnings prospects as it benefits from the robust glove demand in both cleanroom and healthcare sectors. Hower, the house lower TP due to a switch to DCF valuation methodology to better reflect the inflection in selling prices and earnings normalisation in coming years. The house sees dividend yield for FY21F to potentially rise to 13.2% assuming a 60% payout ratio.

• UOB; John Cheong: Maintain BUY with a higher TP of S$1.75. 1Q net profit beat the house estimate by >100% due to higher than expected ASP and net margin, as well as favorable demand-supply dynamics. The house sees Riverstone’s cleanroom gloves as standing a good chance to maintain favorable ASP beyond COVID-19 as unique selling points.

Propnex

•UOB; Adrian Loh: Maintain BUY with a higher TP of S$1.34. 1Q net profit jumped 97% to S$16.2m beating estimates. According to management, the stronger results were due to improved market sentiment, successful COVID-19 vaccine rolls out locally, and availability of ample liquidity, and attractively priced new project launches. While Management believes cooling measures are likely but it will be targeted in nature as the pace of economic recovery remains uncertain.

•CIMB; Lock Mun Yee: Maintain BUY with higher TP of S$1.19, based on 10x FY2021F PE and DCF valuation. The House raised its earnings estimates for FY21-23F by 14.9-21.9% after increasing its private resale and primary market transaction value assumptions due to a higher mix of centrally located products.

For our more info on markets and access to stock research, pls open a trading account with our preferred broker or subscribe to us. PM @moneyplantt at Telegram or email us at connect@gem-comm.com

Join our Telegram, Instagram, Facebook and Linkedin.

I distinctly remember what I felt when I saw my first full-time salary in my bank account.

“Omg…like that only ah…”

I was earning a typical graduate’s pay at that time. After calculating a realistic monthly expenses budget, I realised that I could only save approximately $1000+ each month. It would take me the entire year to save just slightly above $10,000.

What I meant by a realistic budget was this: I was working at an office in Orchard then. There were no hawker centres, and food courts were few and far between. Sure, I could eat at a food court daily, order cai png or fishball noodles and save a ton. But eating that daily? That’s quite a stretch.

Sometimes, my lunch buddies and I just wanted something different for a change. Is that too much to ask for? *grumbles*

That monotomous 9-to-5 life also meant that most office workers will need some entertainment through the work week. Shopping for new work outfits, streaming service subscriptions, a gym membership, weekend activities…the list goes on. Unless you have a difficult and urgent financial situation to deal with, I think that most of us would find it hard to get through the week without any entertainment at all.

I wondered how I was going to pay for big ticket items in the future, like a house, a family, or let’s be real, medical expenses if my parents’ ever needed it. The pressure was real – during work, to meet work expectations, and after work, to meet life expecations.

If you want to increase your foundation of savings faster, here are some tips on how you can do it.

#1 Create a budgeting rule (50/30/20)

Arguably the most popular budgeting rule is the 50/30/20 rule.

You can modify the rule to suit your needs. I can comfortably save about 40% of my earnings. The rule looks more like 40/20/40 for me.

The thing about budgeting rules is that it only works if you stick to it, duh. If you have trouble sticking to budgets, I recommend keeping track of your expenses using an app. I use Wallet, they have a mobile and web version which makes it really convenient to track your expenses even when you’re on the go. There are paid features on the app, but the free one works just fine for me. I can set monthly budgets, create savings goals and track expenses from different bank accounts, which is detailed enough for my purposes.

There’s no trick, no hack for this. Just record everything the moment you spend it and control your expenses if you’ve overspent for a few days.

#2 Know what to spend on

You know how to save, but do you know how to spend?

Honestly, this one takes a bit of trial and error. It’s about knowing your lifestyle and what works for you, and nobody gets it right at the first try.

I used to spend on a monthly gym membership, which I only discovered a few hundred dollars later that it wasn’t for me. Some other things I used to splurge on were things like weekend cafe runs and excessive grab rides. Of course, there are people who save excessively and sacrifice on some enjoyment. How much and what you choose to spend on lies on a spectrum.

That’s why the word is relative. How and what to spend on is entirely up to you. That’s why the hardest part about this all is comparison – feeling like you have to do what the next person is doing. But that’s a conversation for another day.

For a start, be honest with yourself about what works and what doesn’t work, and don’t be afraid to cut things out when they emotional payoff doesn’t match the financial expenses.

#3 Get on the side hustle bandwagon

One way to save more is to earn more. Enter the side hustle life.

Still not convinced by the side hustle life? Just think about the avalanche of uncertainty and change that is 2020. Now’s the time to start diversifying your income streams.

But the side hustle life isn’t all rosy. Side hustling means working more than your regular 9-to-5 hours. You must be prepared to sacrifice time for rest and socialising to do this.

Of course, you might think that you can get a cushy side hustle that pays decently well for a bit of work. However, my experience with side hustles is that it can be a hit or miss. It’s hard to find something that balances out the money vs time equation. I really can’t justify getting paid $10 for a 600 word article (yes, those are the rates you’ll find in low entry writing jobs).

That doesn’t mean it’s impossible. I know of accounting colleagues who did some simple bookkeeping for small business owners, friends who are event photographers on the side. It takes a bit of creativity and a lot of hard work to distill from your existing skillset something that people need.

When you have 6 months of salary in savings, you’re in the clear to begin investing – we will be sharing more about investing tips in future articles. In the meantime, happy saving!

Follow us on Telegram, Instagram, Facebook and Linkedin for more investment tips coming up!

What happened?

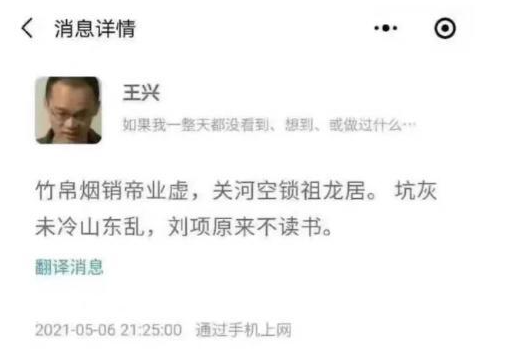

Meituan’s share price dropped as much as 9.8% on Monday after its CEO’s social media post over the weekend sparked concerns that Meituan may face more regulatory crackdown.

|

Meituan CEO cited a poem about burning books during the Qin dynasty in a social media post which sparked speculation that he was complaining about the regulatory crackdown. |

|

Wang has subsequently deleted the post and denied that the post is about the crackdown. In his re-post, he clarified that the post was about the Qin dynasty being wary of scholars, but the ultimate downfall of the Qin Dynasty came down to someone who did not was from Liu Bang who did not read any books. This ancient poem reminded him that the most dangerous competitors are usually not the expected ones- likening the case to Alibaba vs JD.com vs Pingduoduo. |

However, the damage has already been done as Meituan closed 7% down on Monday, closing below HK$274, its recent support, which may suggest further downside from a technical perspective. Meituan is down more than 40% from its 52 weeks high and 10% year to date.

What others are saying?

The post was a very famous anti-establishment poem, which suggests that Meituan may be under huge pressure from the government. It also does not reflect well of Meituan during this period of a crackdown. Sentiments for the China tech sector remain poor as concerns over the government’s regulations continue to linger, and catalysts for market leaders such as Meituan in the near term remain weak.

In terms of valuation, Meituan is attractive as it trades at 7.8x EV/sales- near a 1 year low, after its significant re-rating which started in Mar 2020.

Meituan remains one of the key technology powerhouses, with its dominance in food delivery and online travel booking. However, as price action continues to struggle with ongoing regulatory concerns, are you a bull or a bear for Meituan? Let us know in the comments section below.

Join our Telegram, Instagram, Facebook and Linkedin.

What happened in markets this week, and what are analysts talking about?

![]()

MC Payment

RHB issued its Top 20 small-cap jewels for 2021, and MC Payment was part of this year’s series.

• RHB; Shekhar Jaiswal: MC Payment is the first SGX-listed proxy to growth in the ASEAN digital payments industry, providing an integrated digital payment infrastructure for merchants by offering a one-stop solution to accept all forms of digital payment and enabling them to run their businesses both online and offline. The house believes that MC Payment is a good proxy to e-payment growth in ASEAN, amidst the rising household income and increasing online commerce, underlying the need for economies to go cashless. The house also notes that, MC Payment’s closest ASEAN listed peer, GHL SYstems has seen earnings growth at 33% CAGR, and share price performance of 300% return in 5 years.

Marco Polo Marine

RHB issued its Top 20 small-cap jewels for 2021, and Marco Polo Marine was part of this year’s series.

• RHB; Jarick Seet : The house sees Marco Polo Marine as an Oil and Gas turnaround play having reversed from a loss of S$3.9m in FY18 to a positive EBITDA of S$2.4m in FY19. With a brighter outlook, the house sees a return to profitability in FY20-21F as highly possible with a continued pick-up in ship chartering, and ship repair/building activities. The house sees potential for a strong re-rating for the stock once profitability starts to kick in. Currently, the house believes Marco Polo Marine holds deep value where the Group is in a net cash balance sheet, and currently trading below significantly impaired NAV, and white knights’ and creditors’ entry price.

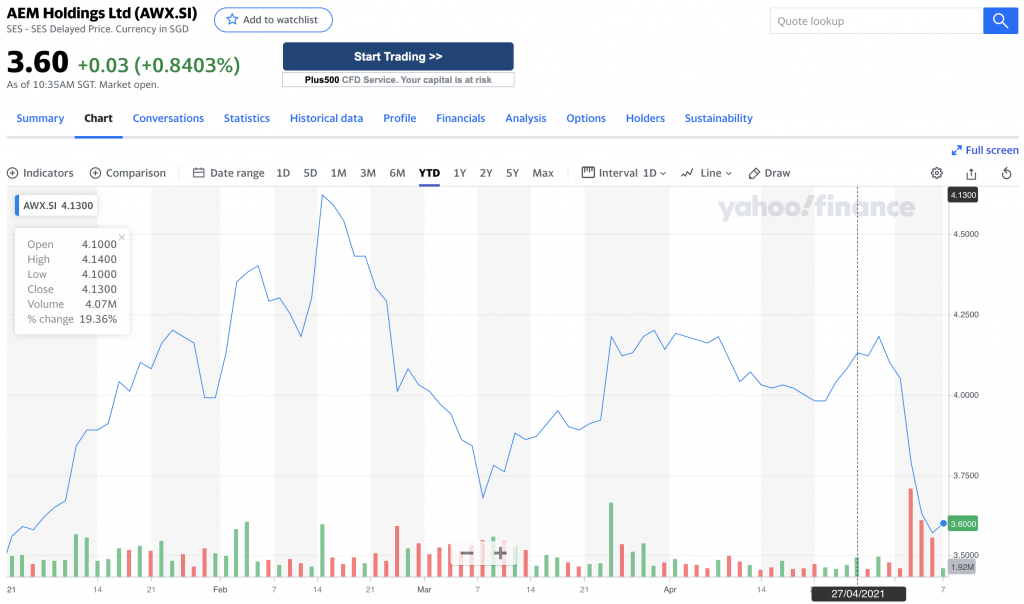

AEM

•Maybank; Gene Lih Lai: 1Q21 net profit was weaker than expected due to tougher comparison year on year, and cyclical softness ahead of volume ramp of new generation test handlers. The house increase TP to S$5.56 to roll forward to 14x FY22F PE, as it believes investors should focus on recovery potential of the Group.

•KGI; Kenny Tan: Maintain Outperform but with lower TP of S$4.36. Believes that long term prospects remain bright but there is limited near term upside to share price. Expect catalysts in 2H21 from potential surprise in orders inflow.

•CIMB; William Tng: Reiterate Add with unchanged TP of S$4.63. AEM expects 1H21 financial performance to be weaker yoy, but guided for a stronger 2H vs 1H. House sees share price weakness as a chance to add.

For our more info on markets and access to stock research, pls open a trading account with our preferred broker or subscribe to us. PM @moneyplantt at Telegram or email us at connect@gem-comm.com

Join our Telegram, Instagram, Facebook and Linkedin.

“We live in a culture of blame. People will blame anyone or anything for their misery sooner than take the responsibility to own it and make it better.” Dr. Henry Cloud; Dr. John Townsend, It’s Not My Fault.

We have met many many investors around the world. There are those who are responsible and there are those who blame anyone and anything.

This is apparent yet often ignored: You are the only person responsible for your investments. You have a mind of your own.

In life, as an investor or not, we must be responsible for our own decision and doings. Even if someone gave you a piece advice or sent some marketing materials – this should just be a reference. If you decide to go ahead and invest, be responsible for your own Losses and Wins.

The Bak Kwa Theory

We put on weight after eating that Bak Kwa (Asian Pork Jerky); we blame it on Bak Kwa’s marketing for that enticing advertisement. The fact is you gave in to temptation!

We have heard many complaints for why and how some investors lost money.

Some of these excuses include:

- “That someone told me it’s a good stock!”

- “The management is a liar”

- “The sell-side analyst suckz”

- “The Investor relations marketed the stock”

- “The blog said it’s excellent stock idea”

And the list goes on.

You lost money- wrong pick, wrong analysis on your own.

If you invest without analyzing or when your original thesis turns out to be wrong — then you are solely responsible!

Be Responsible and Stop the Blame Game

Excuses and blames reflect how lazy and irresponsible we are. We must do all the heavy lifting that’s called homework. If it were capital guaranteed, then everyone would be a wealthy investor. Sorry, life is not all roses!

You won’t believe that Disney founder was fired by his newspaper editor for apparently “not having good ideas or any imagination?” That’s right, his newspaper editor didn’t even believe he can be a good writer. And Disney took the feedback and worked on it. Improvised and Innovate.

Walt Disney Co. is currently valued billions of dollars.

Stop Whining

Whining about bad luck/ bad advises reflects badly on you. I met an investor many years ago. We marketed a Singapore listed entertainment stock to him and he made tons. Unfortunate events happened to the company and the stock tanked due to unforeseen circumstances. He blames everything except for himself about it.

When good times, you enjoyed the harvest. Bad times, you blame everyone and everything except yourself.

A man can lose money, but he isn’t a failure until he begins to blame somebody else.

Be a responsible investor, make sure to do your research thoroughly and make a risk-informed decision on which stocks to buy!

Follow us on Telegram, Instagram, Facebook and Linkedin.

These days, we are inundated with online sales events throughout the year from 1.1 to 12.12. At the time of writing, we are on the eve of 5.5 sales.

The dizzying e-commerce sites and persistent add to cart reminders may be effective for the average shopper, but it certainly did not influence the most stubborn of customers – my mother. Growing up in an Asian family, we were taught to turn a blind eye to sales. There isn’t really a sale, they just want you to spend money, my mother used to say. As a teenager who wanted in on all the latest trends, I must admit I was mildly annoyed at that. However, I fully appreciate the think twice, think thrice mentality that was instilled in me.

So before you check out of your cart today, here are some things to consider (courtesy of my very Asian mother).

1. Quality vs Price

For over 10 years, my parents continued using the same household items. It wasn’t until long later when the items finally reached the end of their life span that they were duly retired.

Back in the day when there wasn’t e-commerce, my parents were great at sourcing out quality products at a reasonable price by browsing through their options dilligently.

These days, the prices of some items have gone down drastically, but so has quality. If you’re fishing for a deal, consider the quality vs price conundrum. Is it worth spending that $5 if what you’re buying will disintegrate after a few uses?

And if you’re eyeing something that’s more expensive…

2. Can it wait?

Because the best sales are usually the year end ones. Think 11.11, Black Friday, 12.12, Christmas and New Year’s sales.

There are some decent discounts this 5.5, but certainly not as impressive as the year end ones. If it isn’t something that’s particularly urgent, it’d do you good to wait till the end of the year before you check out.

3. How long will you use it for?

If you have a room full of stuff lying around, it’s time to reevaluate if you really need more stuff.

What I do is to delay some gratification. It’s always a good idea to wait a little while to see if you really need something; whether it can really add value to you.

I tend to look for value in products, and maybe this is an age thing. Can this improve my quality of life? Can this improve my day to day experiences? Does this make me happy in the long run? Because if it’s only going to end up in a forgotten corner of the house, then it probably isn’t serving you in the long run.

If you’re worried that the product might get sold out – I do think that you can find dupes for most things. As my mother would say, you can always find another company making the same thing.

Happy shopping folks!

What happened?

Ethereum, the second-largest cryptocurrency after Bitcoin, has been stealing the limelight of late. Prices broke above $3,000 to set a new record high, after rising more than 300% year to date.

Year to date market capitalization of Ethereum (USD)

Why did it happen?

According to some crypto experts, they believe this is a catch-up rally by Ethereum (ETH) to the gains of Bitcoin which rallied late last year, with the rise in interest from institutions. However, with ETH’s recent rise, it is now Bitcoin that is now lagging behind. ETH has gained more than 1,400% over the last 1 year vs Bitcoin which has gained more than 500% over the past year. (Still decent gains for both)

Other reasons attributed to the rise of ETH includes

1) The issuance of European Investment Bank’s (EIB) first ever digital bond (EUR 100m 2 year bond) on the ETH blockchain. This sparked a “bullish institutional use case for Ethereum”, following the support by EIB who believed “the digitalization of capital markets may bring benefits to market participants in the coming years, including a reduction of intermediaries and fixed costs, better market transparency through an increased capacity to see trading flows and identity asset owners, as well as a much faster settlement speed.” Click here to see how ETH transactions work.

2) Rising popularity of non-fungible token (NFT), which boosted the demand for ETH as most NFTs are part of the ETH blockchain. NFT are “tokens that we can use to represent ownership of unique items.” and it can be anything that is digital including drawings, songs, etc, where you buy the ownership of the digital asset. The most well-known NFT so far will probably be the sale of the first tweet by Twitter’s founder and CEO, Jack Dorsey, who sold it as an NFT for $2.9 million.

NFTs’ popularity surged in recent years as more people buy and sell digital artwork. Most of the NFT tokens are built on the ETH network which enable NFT to work due to the reasons below (as quoted from ethereum.org)

- Transaction history and token metadata is publicly verifiable – it’s simple to prove ownership history.

- Once a transaction is confirmed, it’s nearly impossible to manipulate that data to “steal” ownership.

- Trading NFTs can happen peer-to-peer without needing platforms that can take large cuts as compensation.

- All Ethereum products share the same “backend”. Put another way, all Ethereum products can easily understand each other – this makes NFTs portable across products. You can buy an NFT on one product and sell it on another easily. As a creator you can list your NFTs on multiple products at the same time – every product will have the most up-to-date ownership information.

- Ethereum never goes down, meaning your tokens will always be available to sell.

So will Ethereum continue to rise? We are in the bull camp for ETH as in addition to being a cryptocurrency, ETH actually offers functionalities such as smart contracts which are starting to gain the traction and support from major institutions and sectors. Hopefully as the number of use cases increase, so will the price. Go ETH Go Go Go!

Are you a ETH bull or bear? Let us know in the comments section below!

Join our Telegram, Instagram, Facebook and Linkedin.

If you’re like me, your head would start spinning the moment finance terms are thrown out in conversations. Unfortunately though, there comes a time when you’ll have to take the finance Panadol if you want to be serious about adulting.

So I’ve taken it upon myself to unravel the definitions of these common finance terms, and explain them to you in the way a finance noob can understand.

I remember first hearing the terms asset and liability back in a basic financial literacy course in school. Given that my financial horizon was only as far as my monthly allowance, it was difficult to grasp economic losses and gains as long as 10 years later. With age (and plenty of adulting), I’m happy to report that that has changed.

First, let’s look at assets.

Assets – what you have

In simple terms, assets are the things that can provide economic value for you. Time is of the essence here. Assets can be classified into two broad categories: current assets and fixed assets.

Current assets include things like cash, inventory – items that can be converted into a cash easily.

Fixed assets refers to long term assets, such as property and equipment, items that cannot be converted into cash quickly.

Liability – what you owe

Liabilities are your debts – mortgage debt, bank debt, taxes owed.

Likewise, there generally two types of liabilities: current liabilites or long-term liabilities.

Current liabilities refers to debts that need to be paid typically within a one year period. These include employee payroll, or an upcoming payment to a vendor.

Long-term liabilities includes things like a bank debt that is payable over a 10 year period.

Simple enough? Not quite.

The time factor

This is where the definition of asset vs liability becomes a little grey. While some pay consider property an asset, that is only on the assumption that you make money from it after a sale. Especially if you the property is your current residence, it’s unlikely that you will sell it in the short term. Putting a future value on fixed assets becomes tricky because there can be market shifts that are hard to predict. Case in point: the current pandemic situation today.

Knowing how to classify which items into which basket on your balance sheet is an important financial management skill to have. Maintaining more assets than liabilities is the hallmark of any good personal or business financial management.

Stay tuned for more finance terms coming your way next week!

What happened in markets this week, and what are analysts talking about?

Meituan

The Chinese State Administration for Market Regulation has launched investigations on Meituan over alleged monopolistic behaviors. Meituan has previously been criticized by rivals and merchants for their alleged excesses such as forced exclusive arrangements and had previously also been found guilty of unfair competition where Meituan was ordered to pay compensation to its rival, Alibaba’s Ele.me in food delivery.

• Goldman Sachs: Meituan has published a statement saying that the Group will actively cooperate with regulators to further improve compliance with the regulations. During the recent briefing, Meituan stated that it has been actively adjusting business practices including the modification of how it charges merchants, separate transaction services, and actual on-demand delivery charges to help create a healthier transparent charging environment.

•CIMB: Meituan’s total FY20 sales was RMB115b. The amount of fine is estimated to be RMB1.15-11.5b (1-10% of total sales), representing 20-197% of the House’s FY21F adjusted net profit. Previous monopoly investigation towards Alibaba has lasted 3-4 months.

•UBS: Not surprised by the announcement. Believe Alibaba’s recent investigation could be a good benchmark, and if Meituan is fined also 4% of last year’s business unit revenue, its potential fine could be RMB2.7b. (If it includes store business, the potential fine could be 24% higher). Excluding recent raise of US$10b, Meituan had RMB61.1b cash and short-term investments. Still like Meituan for its long-term growth prospects, and with prices down 31% from recent peak vs Alibaba’s down 27%, suggesting investors have priced in some regulatory concerns. A conclusion to the investigation could be a positive catalyst.

![]()

mm2 Asia

• UOB Kayhian; Lucas Teng/John Cheong: Initiate coverage on mm2 Asia with a SOTP target price of S$0.098. mm2 is trading at 0.6x P/B and inexpensive FY20 earnings (pre-COVID-19). Concerns over the Group’s cinema business could be slowly lifted with: a) improved seating capacity, b) a potential spin-off, and c) a potential merger with Golden Village, while the overhang from its high debt levels has also been addressed. The group has recently completed a rights issue of approximately S$54.7m which reduces net gearing to approximately 0.8x (vs 1.0x previously) and enables interest savings with the repayment of a medium-term note. There is also a possible spin-off for the cinema business, in which convertible bonds of S$47.9m will be converted to equity in the listed cinema entity. If the cinema IPO materializes, this will further reduce the group’s net debt level to 0.4x.

Singapore Exchange

• UOB Kayhian; Lucas Teng: Initiate Coverage on SGX with Buy recommendation and Target Price of S$12.35. SGX is benefitting from structural tailwinds including the electronification of OTCs and passive investing. Potential catalysts may include Singapore-based secondary listing of foreign listed entities such as Grab or SEA ltd.

For our more info on markets and access to stock research, pls open a trading account with our preferred broker or subscribe to us. PM @moneyplantt at Telegram or email us at connect@gem-comm.com